Now and Then – A ‘Tightwad’ at the Fed

While the current administration struggles to figure out their position on inflation, forcing Treasury Secretary and former Federal Reserve Chair Janet Yellen into an uncomfortable “mea culpa” and current Fed Char Jerome Powell into a pointless public relations photo op, let’s take a look back at our last major inflationary crisis as a point of comparison with my commentary in bold italics.

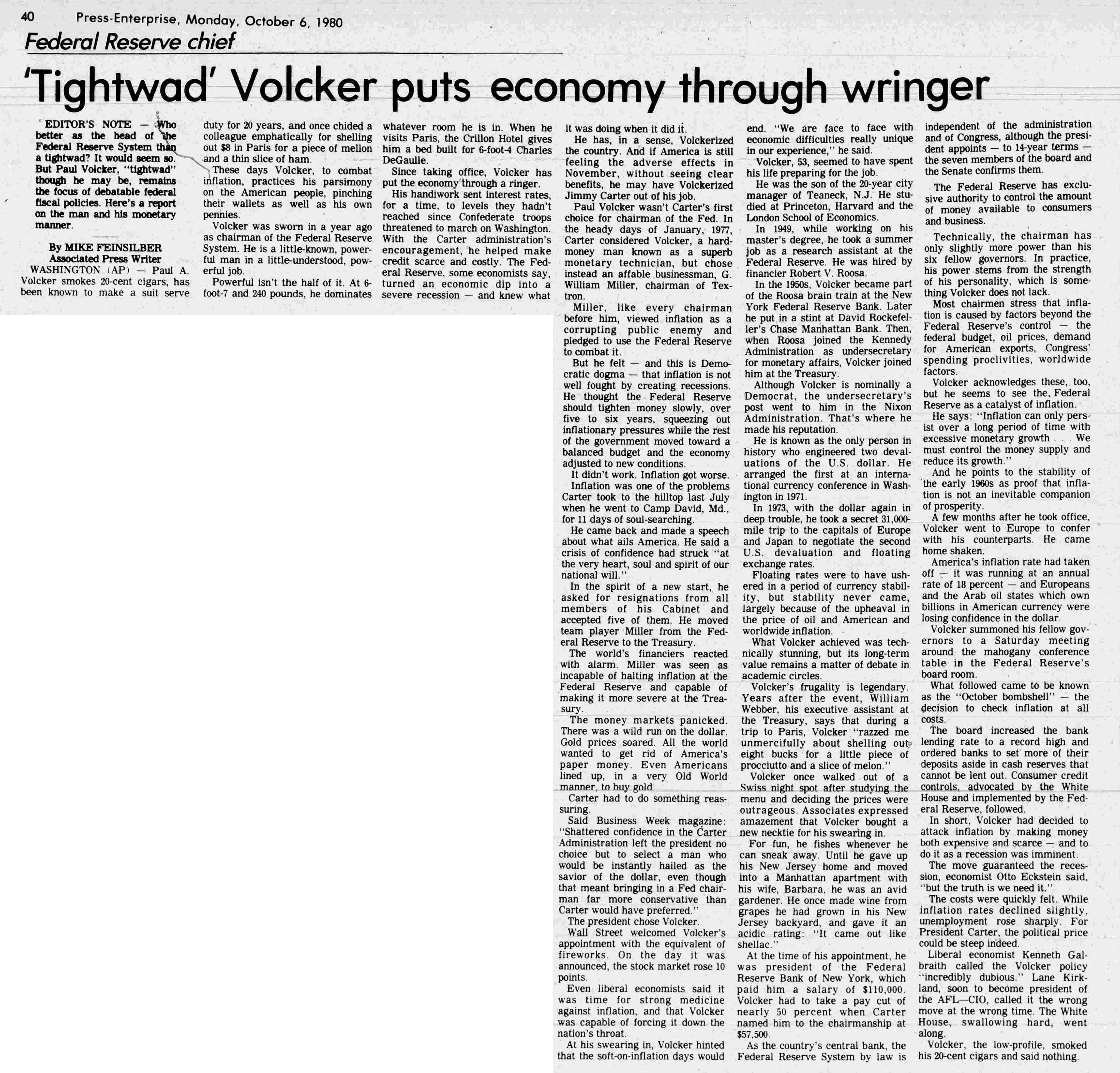

In October of 1980, a headline read “’Tightwad’ Volcker puts economy through the wringer” with the author detailing some of the Federal Reserve Chair Paul Volcker personal habits and opining that his handiwork had brought interest rates up to a level not seen since Confederate troops threatened to march on Washington. Further, it was noted by Business Week that “Shattered confidence in the Carter Administration left the president no choice but to select a man who would be instantly hailed as the savior of the dollar, even though that meant bringing in a Fed chairman far more conservative than Carter would have preferred.”

By contrast, today, the Biden administration is just beginning to recognize how far they are behind the curve. When Jimmy Carter nominated Volcker, it was an admission of defeat while today Biden is just beginning to recognize that a fight is on.

In March of 1981, another headline reads “L.A. bank raises prime to 17.5” with the author indicating that various banks were bringing their prime lending rates up by 0.5% as a result of “sharp” increases in the Federal Funds Rate and detailing that “Last week, federal funds were trading as low as 13 percent, but the rate jumped above 15 percent this week.” Further it was noted by a Security Pacific (the L.A. bank) spokesman that “The federal funds rate has gone up 200 basis points and CD rates about 100 basis points,”

The Federal Funds rate jumping by 200 basis points over the course of a few weeks offers a truly comical contrast to today’s endless worry and handwringing over the Feds prospect of going 25 or 50 bps at the next meeting. Clearly, we are more attuned to and afraid of the impact that increasing interest rates will have on our asset prices likely as a result of being essentially less resilient and more fearful overall.

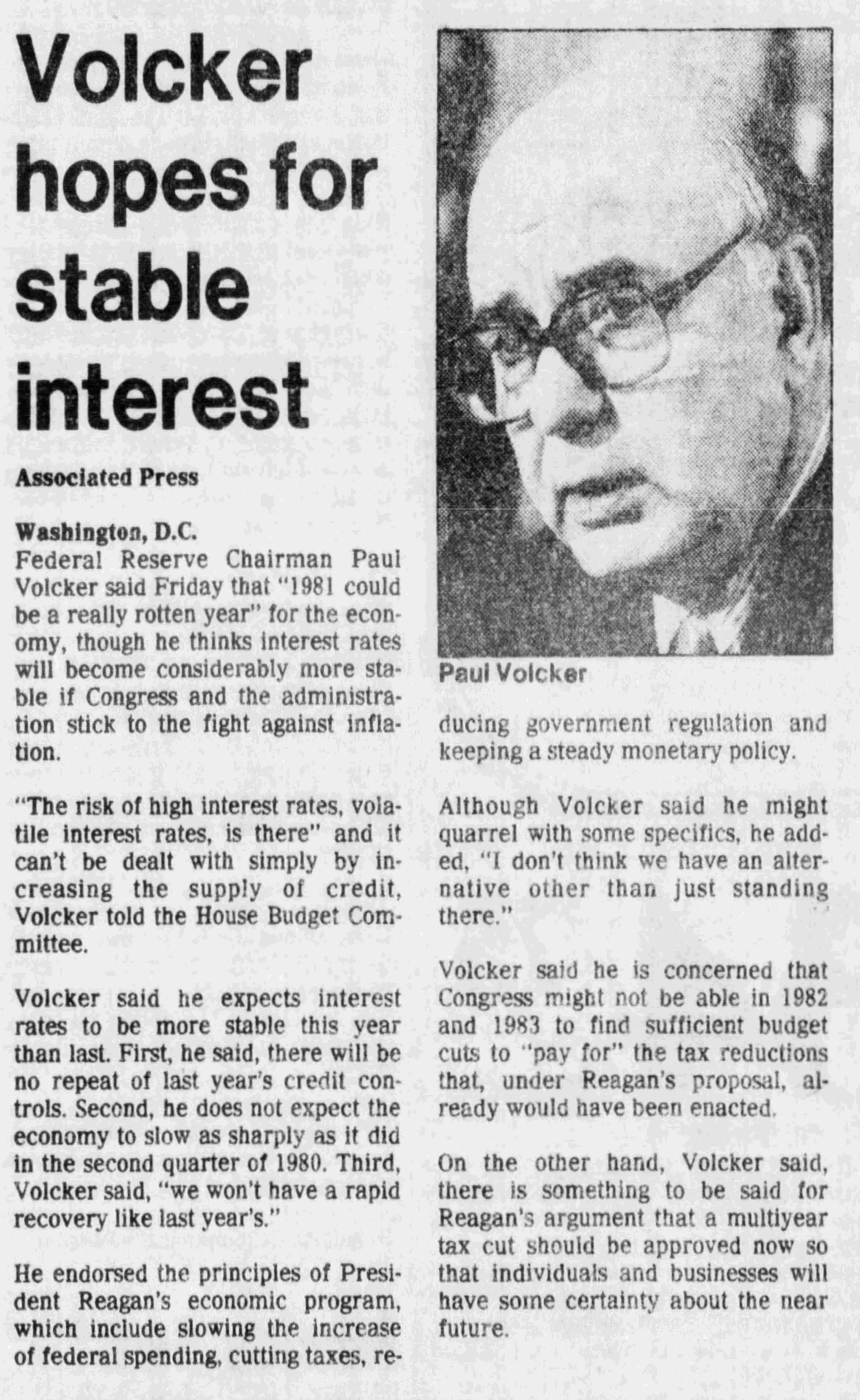

Another March of 1981 headline reads “Volcker Hopes for Stable Interest” within which Fed Chair Paul Volcker is quoted as saying “1981 could be a really rotten year” for the economy indicating further that “The risk of high interest rates, is there” and further still that “we won’t have a rapid recovery like last year’s.”

Clearly, the early 80s were a very different time. We now find ourselves in an era where a slight wrong choice of words by even just a random member of the FOMC sends world markets reeling.

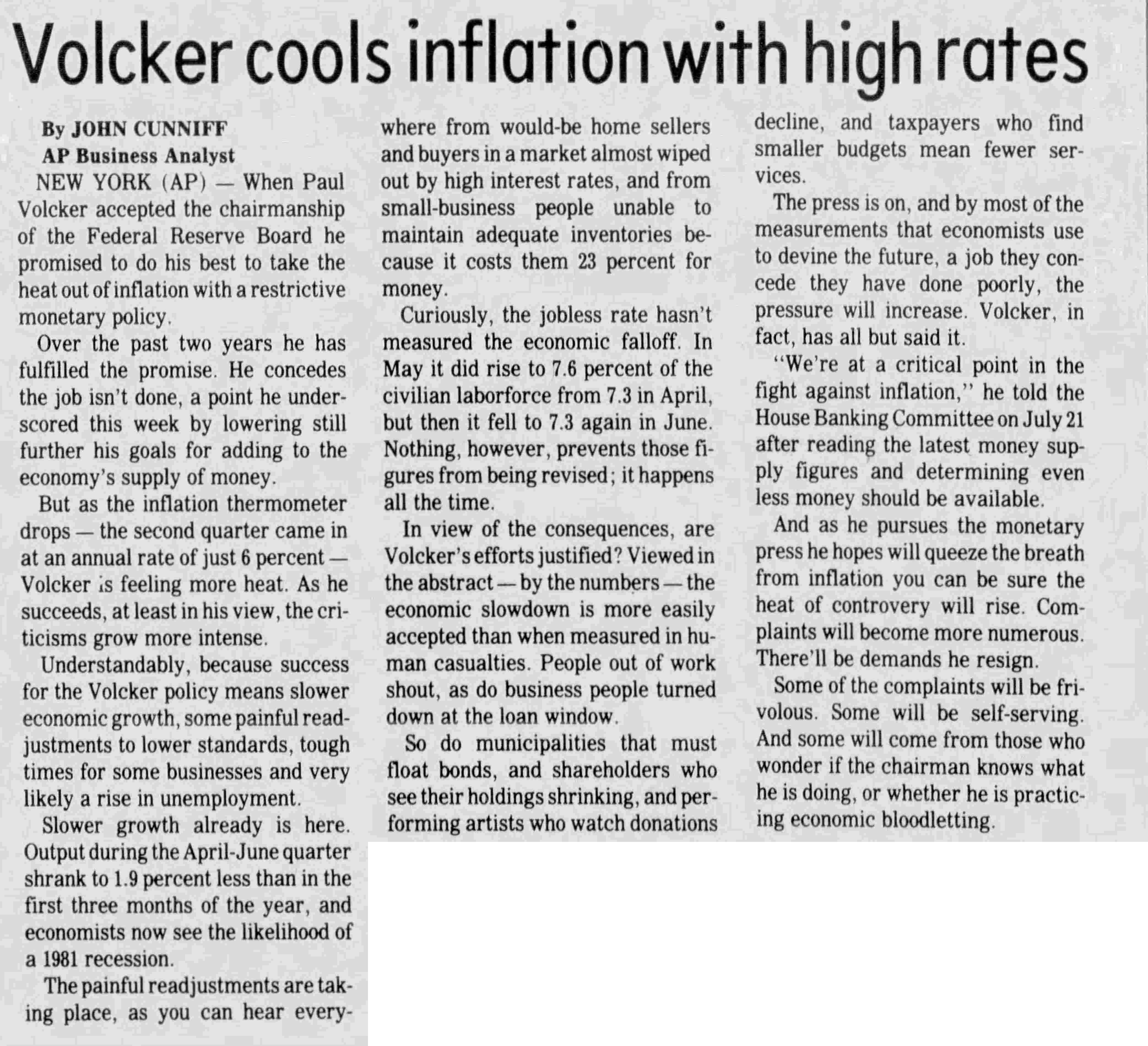

Finally, a July of 1981 headline reads “Volcker cools inflation with high rates” within which it is detailed that “The painful readjustments are taking place, as you can hear everywhere from would-be home sellers and buyers in a market almost wiped out by high interest rates, and from small-business people unable to maintain adequate inventories because it costs them 23 percent for money” and concludes “Some of the complaints [about the Feds course of action] will be frivolous. Some will be self-serving. And some will come from those who wonder if the chairman knows what he is doing, or whether he is practicing economic bloodletting.”

After two years with a Federal Reserve engaged in a pitched battle with inflation pushing the U.S. into one recession and on the brink of a second (that was to materialize later that year), there was significant uncertainty about the path forward as notable pain was being felt by households and firms.

Fighting persistent monetary inflation is not just a simple nominal policy course correction; it is a fundamental process of tightening the monetary system by severely contracting the money supply and thoroughly disabusing all market participants of any ideas that the old easy-money regime will ever return.